Imagine looking at a financial model that clearly shows your cash reserves dropping every thirty days. Your user graph points up and to the right. The revenue line is growing steadily. Yet the gap between cash going out and cash coming in refuses to close. You are scaling rapidly. Are you actually building a business or just heavily subsidizing your customers?

This is the reality of being default dead.

We spend years being told that momentum is the only thing that matters. You raise money, you spend it to acquire users, and you raise more money on the promise of that larger user base. It is a loop that works flawlessly when macroeconomic conditions are highly favorable. But what happens when the funding environment cools down and investors start asking about profitability?

Suddenly, the music stops. You are left holding a machine that consumes more fuel than it produces.

The Mathematics of Survival

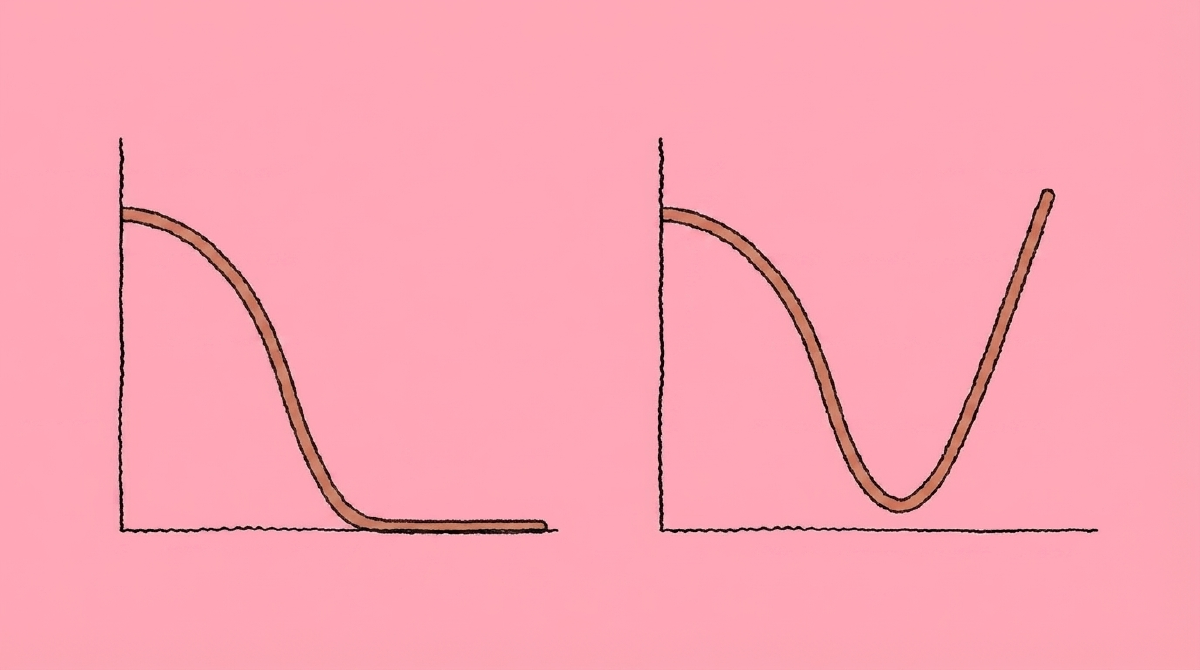

#The concept of default dead versus default alive was popularized by Y Combinator founder Paul Graham. The calculation is deeply pragmatic. You take your current expenses and your current revenue growth rate. Assuming those remain constant over time, do you reach profitability before your bank balance hits zero?

If the answer is no, you are default dead.

If the answer is yes, you are default alive. For a long time, being default dead was an accepted stage of early company building. Capital was cheap. Investors rewarded aggressive expansion over sustainable margins. It made logical sense to capture market share first and figure out the margins later. We are now operating in a very different reality.

Economic downturns force a harsh light onto the fundamental mechanics of your operations. If external capital is no longer a reliable safety net, the internal engine of your business must sustain itself.

How exactly do you rewire a company built for speed to suddenly prioritize efficiency?

Interrogating Your Unit Economics

#The pivot begins at the atomic level of your business. You have to strip away the aggregate numbers. Total revenue and total active users can easily mask fatal flaws in how your company operates. You need to examine your unit economics. This means looking at the specific costs and revenues associated with a single customer.

Are you making more money on a single transaction than it costs to deliver that transaction?

To answer this, we have to look at several specific inputs:

- Customer Acquisition Cost: The exact dollar amount required to convince someone to buy your product, including sales and marketing overhead.

- Lifetime Value: The gross margin you expect to earn from that customer over their entire relationship with your business.

- Payback Period: The number of months it takes to recover the acquisition cost from a specific customer.

- Variable Costs: The operational expenses that scale directly with the delivery of your product or service.

These metrics are notoriously difficult to track with precision. Founders often blend fixed costs and variable costs together. Many underestimate the true cost of acquiring a customer by leaving out sales salaries or software tools.

When the economy squeezes, these minor accounting illusions become existential threats. You must ask hard questions about your current data. Is your customer acquisition cost rising because the market is crowded, or because your product lacks organic demand? Is your lifetime value shrinking because your customers are cutting their own budgets?

Executing the Strategic Pivot

#Knowing your math is broken is only the first step. Fixing it requires intense operational discipline. The immediate reaction for most leadership teams during a downturn is to cut the burn rate. They reduce headcount, slash marketing budgets, and cancel unused software subscriptions.

Lowering expenses extends your runway.

Cutting costs alone cannot save you.

If your unit economics are fundamentally negative, selling more of your product simply drains your bank account faster. You have to change the equation at the source. This often means making difficult decisions that will intentionally slow your growth.

You might have to raise prices to ensure adequate margins. You might need to fire unprofitable customer segments that demand high support resources but yield low revenue. You may have to shrink the scope of your product to focus purely on the core features that drive direct value for the user.

Pivoting to default alive is an exercise in prioritization. You are actively choosing survival and autonomy over vanity metrics. It requires looking at the business not as a vehicle for a future funding round, but as a standalone entity that must generate more cash than it consumes.

When you make this shift, the daily operations change completely. Product development focuses on efficiency and retention rather than flashy acquisition tools. Sales teams are incentivized on margin rather than raw transaction volume.

The Unknown Variables of a Downturn

#Even with precise calculations and disciplined cuts, we must acknowledge the variables we cannot easily control. Operating in a difficult economy introduces secondary effects that cascade through a business model.

If you successfully pivot your operations to achieve positive unit economics, how do you defend those margins when your software suppliers raise their prices? How do you project lifetime value when historical data is no longer relevant to current market conditions?

There are complex behavioral unknowns as well. Startups are culturally wired for rapid expansion. When a founder stands in front of the company and announces a pivot from growth to sustainability, the psychological shift can be jarring.

How do you maintain team morale and retain top performers when the narrative changes from dominating the market to simply surviving the year? Does the culture shift from optimism to anxiety?

These are questions that financial models cannot answer. They require a specific type of leadership that relies on transparency and a clear presentation of the facts.

Regaining Control of the Future

#Reaching a state of default alive completely alters the psychology of a founder. When your runway is theoretically infinite, desperation leaves the room. You no longer have to raise capital on unfavorable terms just to keep the lights on. You can choose to raise money to accelerate a proven and profitable engine, or you can choose to grow organically at your own pace.

The transition is undeniably painful. It requires breaking down the assumptions you held when you started the business. It forces you to look at your product through the cold lens of margin and acquisition costs.

Yet, this painful audit is exactly what separates companies that merely exist from companies that last. It forces us to ask a final question about our own ventures. If we strip away the venture capital and the industry hype, do we have a machine that actually works?

Answering that question honestly is the first step.