Pre-money valuation is the agreed-upon value of a company immediately before a new round of investment is made. In the landscape of startup fundraising, this figure is the starting line for any negotiation regarding equity.

It dictates the price per share. More importantly, it determines exactly how much of the company the founder must sell to get the cash they need.

For an early-stage founder, this number is often abstract. Unlike a public company with a stock price, a private startup does not have a market cap dictated by millions of trades every day. The pre-money valuation is a theoretical value based on potential rather than historical financial performance.

The Art of Valuation

#Determining pre-money valuation is more art than science, especially in the Seed or Series A stages. Since there may be little to no revenue, investors cannot rely on standard EBITDA multiples.

Instead, the number is derived from several qualitative factors:

- The Team: The track record and capability of the founders.

- The Market: The total addressable market size.

- The Product: The status of the technology and intellectual property.

- Comparables: What similar startups in the same sector are being valued at.

This subjectivity creates a wide variance in outcomes. We have to ask ourselves if we are valuing the business based on what it is today or what we promise it will be tomorrow.

Pre-Money vs. Post-Money

#The most common point of confusion occurs between pre-money and post-money valuations. It is vital to distinguish between the two to avoid accidental dilution.

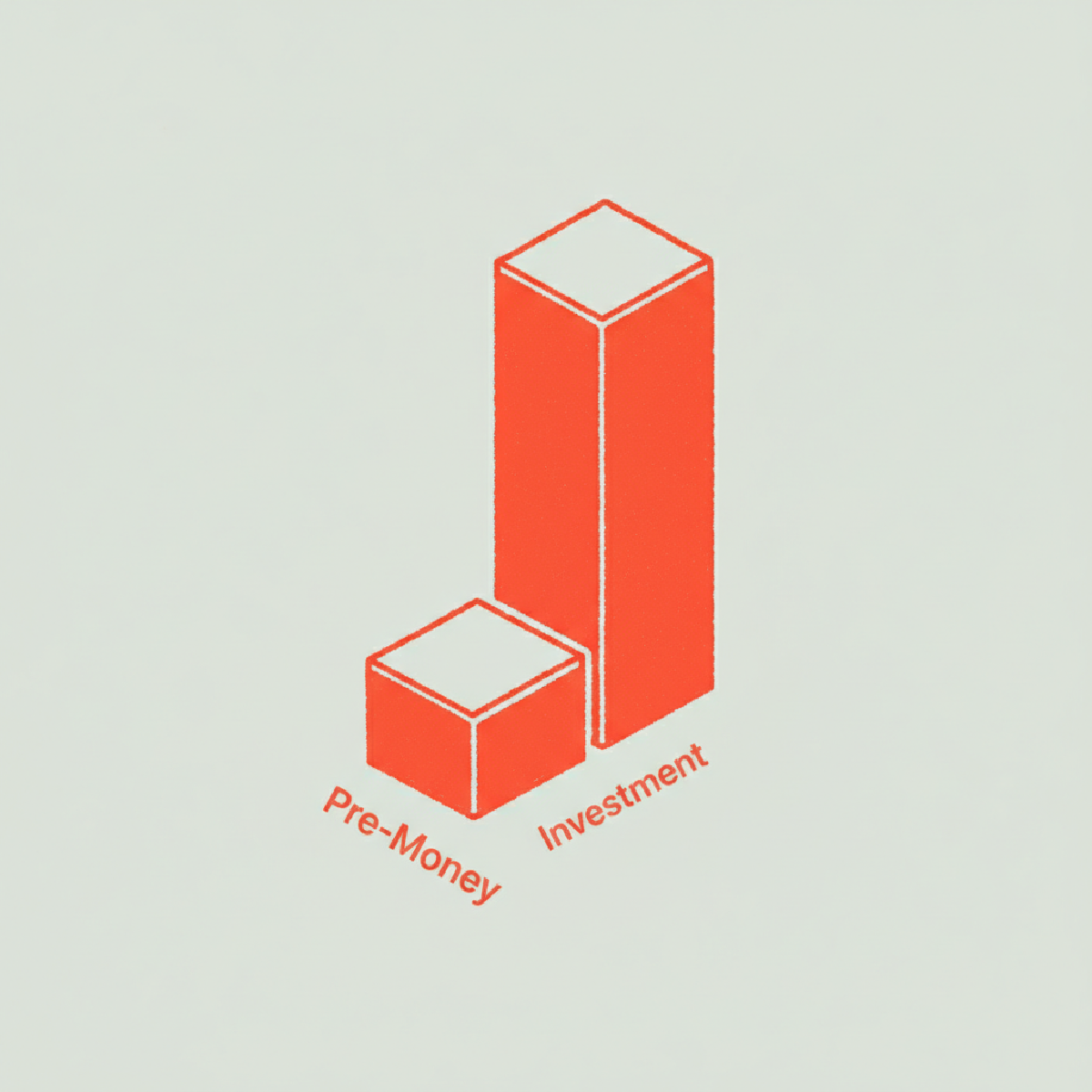

The relationship is defined by a simple equation. Pre-Money Valuation plus Investment equals Post-Money Valuation.

If you have a pre-money valuation of 4 million dollars and you raise 1 million dollars, your post-money valuation is 5 million dollars.

The investor’s ownership is calculated by dividing the investment by the post-money valuation. In this case, 1 million divided by 5 million equals 20 percent.

If a founder mistakenly thinks the 4 million dollar valuation is the post-money figure, the math changes. The pre-money would actually be 3 million dollars. This would mean selling 25 percent of the company instead of 20 percent.

Strategic Scenarios

#Founders generally want the highest pre-money valuation possible. A higher valuation means you give up less equity for the same amount of cash. This preserves your ownership stake.

However, there are scenarios where a high pre-money valuation can be dangerous.

If the valuation is too high relative to the company’s progress, it sets a very high bar for the next round of funding. To raise money again, you usually need to show growth on top of the previous valuation.

If you cannot justify that high price tag later, you may be forced into a down round. This is where you raise money at a lower valuation than the previous round, often triggering anti-dilution clauses that can severely hurt early shareholders.

Is it better to take a slightly lower valuation now to ensure a beatable benchmark for the future? That is a question every founder must weigh against the immediate pain of dilution.